How to handle money the right way?

- Anushree Koppikar

- Sep 20, 2023

- 2 min read

Handling money after getting your first job is an important step in achieving financial stability and security. Here are some steps to help you manage your money effectively:

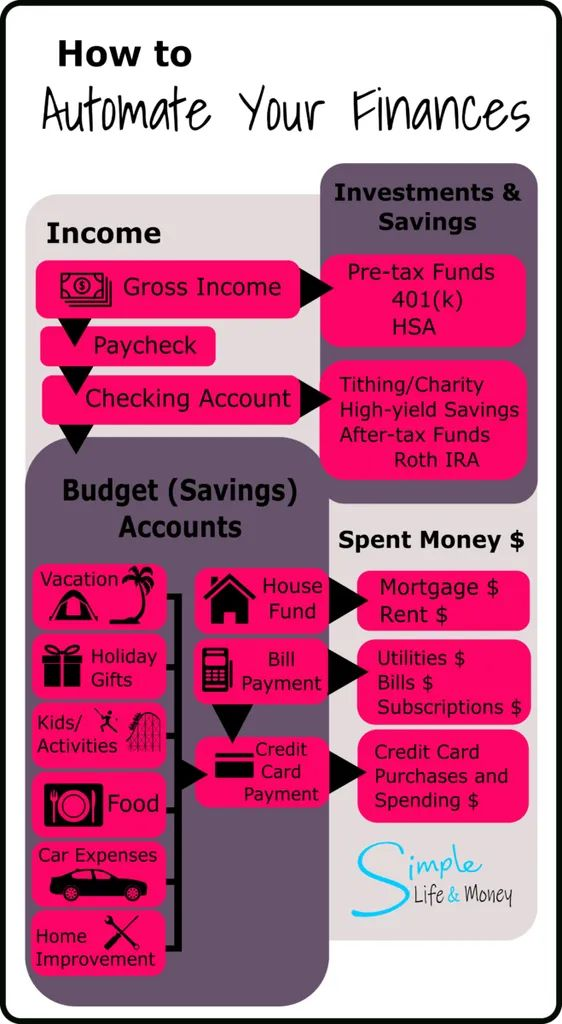

1. Create a Budget:

Start by listing all your sources of income, including your salary.

Make a list of your monthly expenses, including rent or mortgage, utilities, groceries, transportation, and any other regular bills.

Allocate a portion of your income for savings and investments.

2. Set Financial Goals:

Define short-term and long-term financial goals, such as saving for an emergency fund, paying off student loans, buying a car, or saving for retirement.

Having clear goals will help you prioritize your spending and stay motivated to save.

3. Build an Emergency Fund:

Aim to save at least three to six months' worth of living expenses in an easily accessible account. This fund will provide a safety net in case of unexpected expenses or job loss.

4. Pay Off Debt:

If you have student loans or credit card debt, prioritize paying them off. High-interest debts should be your first focus.

Make minimum payments on all debts while directing extra funds towards the debt with the highest interest rate.

5. Save for Retirement:

If your employer offers a retirement savings plan (e.g., 401(k)), consider enrolling and contributing enough to take advantage of any employer-matching contributions.

If your employer doesn't offer a retirement plan, open an Individual Retirement Account (IRA) and start saving for your future.

6. Automate Your Savings:

Set up automatic transfers from your checking account to your savings or investment accounts. This ensures that you consistently save and invest without thinking about it.

7. Live Within Your Means:

Avoid the temptation to overspend, especially on non-essential items. Stick to your budget and avoid accumulating unnecessary debt.

8. Build Credit Responsibly:

Use credit cards wisely by paying your bills on time and in full each month. Building good credit will be beneficial in the long run.

9. Invest Wisely:

Once you've established an emergency fund and paid off high-interest debts, consider investing in stocks, bonds, or mutual funds to grow your wealth.

If you're new to investing, consider seeking advice from a financial advisor or using online resources to educate yourself.

10. Track Your Finances:

Regularly review your financial situation, track your expenses, and adjust your budget as needed to meet your goals.

11. Plan for Taxes:

Understand your tax obligations and take advantage of any tax-saving opportunities, such as retirement account contributions or tax deductions.

12. Seek Financial Education:

Continue learning about personal finance to make informed decisions about your money. There are many books, websites, podcasts, YouTube videos, and courses available to help you improve your financial literacy.

Remember that financial success takes time, discipline, and patience. It's essential to stay committed to your financial goals and make adjustments as your circumstances change. Consulting with a financial advisor can also provide valuable guidance tailored to your specific financial situation and goals.

Comments